With KENSTONE you are choosing an experienced, independent partner who can provide you with comprehensive expertise in all areas of property valuation. Below you will find an overview of our fields of activity.

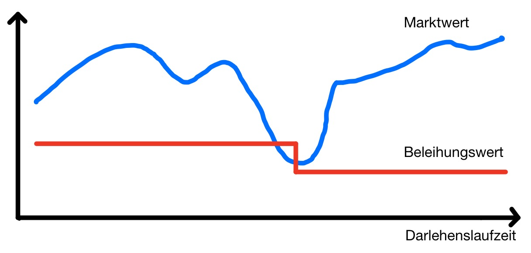

The Mortgage Lending Value concept was first implemented when the Mortgage Banking Act (HBG) was introduced in 1900. In the course of the replacement of the HBG by the Pfandbrief Act (PfandBG) in 2005, the provisions for determining the Mortgage Lending Value was also incorporated into a uniform set of rules with the introduction of the "Ordinance on the determination of the mortgage lending values of land according to §16 (1) and 2 of the Pfandbrief Act" (Mortgage Lending Value Determination Ordinance - BelWertV). The philosophy of the Mortgage Lending Value is that such an established value must be obtained over the entire term of the loan, regardless of the natural market fluctuations, in the hands-free resale of the property. The Mortgage Lending Value is therefore significantly lower than the market value at the time of the calculation and must not be subject to a positive value adjustment during the entire loan term. Regulatory requirements require that market value and Mortgage Lending Value be monitored at regular intervals. In the event of unusually strong negative market fluctuations, the Mortgage Lending Value must also be checked and, if necessary, reduced. A subsequent increase in the Mortgage Lending Value after the market recovery is beginning is not possible.

Graphic showing the market value (Marktwert) in relation to the Mortgage Lending Value (Beleihungswert) and the loan term.

Why do you need the Mortgage Lending Value?

The Mortgage Lending Value is used by the banks as a measure for determining the maximum loan amount for the acquisition of real estate and for determining the loan conditions. The aim of the introduction of an Mortgage Lending Value was to use a carefully determined value for real estate financing, which would be achieved over the entire financing period in the hands-free sale of the property. Banks can refinance themselves at loan levels up to 60% of this value by issuing covered bonds (Pfandbriefe). Pfandbriefe, on the other hand, are regarded as a coin-safe investment with the highest degree of creditor protection. Non-Pfandbrief banks also use the Mortgage Lending Value as a collateral value for determining their loan terms. As part of the financing of real estate, a market and Mortgage Lending Value assessment is therefore regularly commissioned by the financing institute.

How is the Mortgage Lending Value determined?

The determination of the Mortgage Lending Value is based on the procedural rules for determining the market value of a property, with the difference that the valuation must in principle comply with the two-pillar principle and that the legislator defines strict specifications for minimum rates and ranges of the value parameters used. Certain methodological facilities are only allowed by the legislator in the case of evaluations for objects that are financed within the small loan limit (currently € 600,000 incl. all precharges). The two-pillar principle states that a second valuation method must still be used as a benchmark to determine the actual value of the property (comparison value / replacement cost value / income value). The specified ranges for value parameters concern, for example, the object type-specific approaches to useful life, the recognition of maintenance costs, administration costs, rental loss risk, rental income, minimum rates for capitalization as well as further minimum safety discounts and are, especially in strong market phases, decisive for the often significant deviation of the Mortgage Lending Value from the market value of the property. As part of the valuation, the assessor must visit the property (indoor and outdoor inspection) and confirm the pan identity by examining the location, construction and, if necessary, division plans as well as the information in the land register.

Who determines the Mortgage Lending Value?

§16 PfandBG para. 1 stipulates that the valuation, which is used to determine the Mortgage Lending Value, is to be carried out "by an expert independent of the credit decision, who must have the necessary professional experience and the necessary specialist knowledge for the assessment of the Mortgage Lending Value". According to § 6 BelWertV, assessors must meet the more precisely defined requirements: "The expert must have special knowledge and experience in the field of property valuation after his training and professional activity. A corresponding qualification is presumed for persons who have been appointed or certified by a state-recognized or DIN EN ISO/IEC 17024 accredited body as experts or assessors for the valuation of real estate. In selecting the expert, the Pfandbrief Bank has to convince itself that, in addition to many years of professional experience in the valuation of real estate, the expert has in particular the knowledge necessary for the preparation of Mortgage Lending Value assessments, in particular with regard to the respective real estate market and the type of property." As a further prerequisite, the assessor must be independent of the credit acquisition and credit decision process as well as of property mediation, sale and rental (§ 7(1) BelWertV). The use of an opinion submitted or commissioned by the borrower (§ 5 (2) BelWertV) is excluded. The more than 50 HypZert-certified experts of KENSTONE GmbH at 8 locations in Germany fulfill the above requirements. With our extensive expertise in determining the value of the loan, we are happy to assist you in all evaluation questions.